When starting mutual fund investing, many beginners often get confused between:

Lump Sum investing and SIP investing.

Questions like:

- Which option is better?

- Is SIP safer?

- Can lump sum generate higher returns?

- Which method is suitable for beginners?

are very common.

The truth is that both SIP and lump sum investing have their own advantages depending on:

- financial goals,

- market conditions,

- investment amount,

- and risk comfort.

In this guide, let’s understand Lump Sum vs SIP in simple and beginner-friendly language.

What is Lump Sum Investment?

Lump sum investing means:

investing a large amount of money at one time.

For example:

- investing ₹1 lakh together into a mutual fund.

Instead of investing monthly, the full amount is invested immediately.

Lump sum investing is commonly used when investors already have:

- savings,

- bonus income,

- inheritance,

- or surplus funds available.

What is SIP Investment?

SIP (Systematic Investment Plan) means:

investing fixed amounts regularly over time.

For example:

- ₹2000 every month,

- ₹5000 every month,

- or ₹10,000 monthly.

SIP spreads investments gradually across different market conditions.

This is why SIP is often considered beginner-friendly.

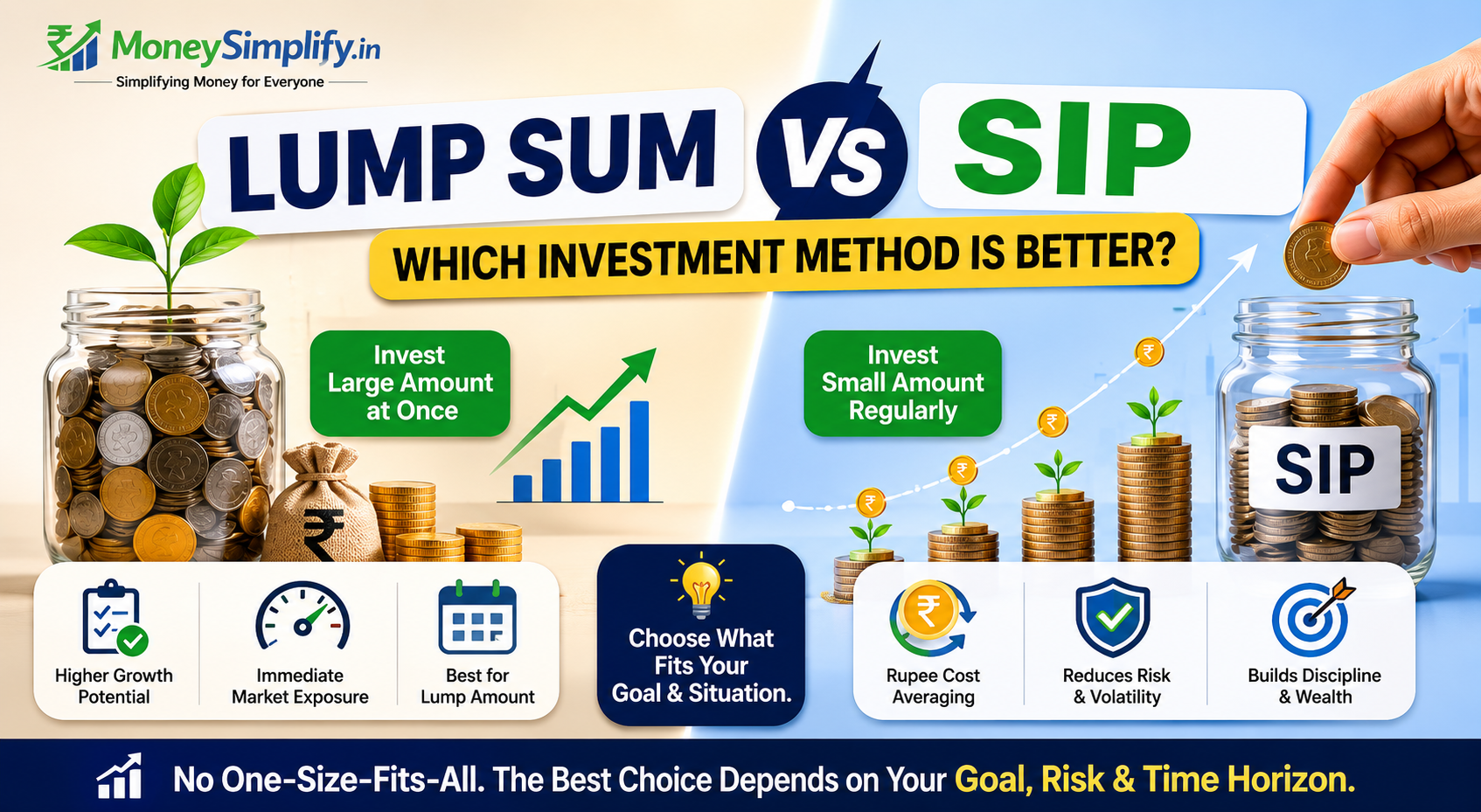

Lump Sum vs SIP — Quick Comparison

| Feature | Lump Sum | SIP |

|---|---|---|

| Investment Style | One-time investment | Regular monthly investment |

| Market Timing Importance | Higher | Lower |

| Risk Level | Higher during volatile markets | Comparatively lower |

| Suitable For | Investors with large funds | Beginners and salaried individuals |

| Investment Discipline | Less structured | Highly disciplined |

| Flexibility | Moderate | High |

| Emotional Pressure | Higher | Lower |

How Lump Sum Investing Works

In lump sum investing:

- the entire investment amount enters the market immediately.

This means:

- returns depend heavily on market conditions at the time of investment.

If markets perform well after investment:

- returns may become strong.

However, if markets decline:

- short-term losses may occur.

Because of this, lump sum investing usually requires:

- higher risk tolerance,

- and better emotional control.

How SIP Investing Works

SIP invests money gradually over time.

Since investments happen regularly:

- investors buy units at different NAV levels,

- market timing pressure reduces,

- and emotional investing may decrease.

This process contributes to:

rupee cost averaging

which may help reduce the impact of market volatility over long periods.

Which is Better for Beginners?

For many beginners:

SIP is often considered more beginner-friendly.

Reasons include:

- smaller starting amounts,

- disciplined investing,

- reduced market timing stress,

- and gradual investing habit development.

SIP is especially useful for:

- salaried individuals,

- first-time investors,

- and long-term wealth builders.

When Lump Sum May Be Suitable

Lump sum investing may be suitable when:

- markets appear reasonably valued,

- investors have large idle funds,

- or long-term investment confidence is strong.

However, market timing remains important in lump sum investing.

Risk Comparison

Lump Sum Risk

Since the full amount enters the market immediately:

- short-term volatility may affect investments more strongly.

SIP Risk

SIP spreads investments over time, which may help reduce the effect of market fluctuations.

However, SIP is still market-linked and not risk-free.

Returns Comparison

There is no fixed answer to:

“Which always gives better returns?”

Sometimes:

- lump sum may outperform SIP during strong market rallies.

Other times:

- SIP may provide smoother investment experience during volatile markets.

Investment duration and market conditions both play important roles.

Emotional Investing Difference

One underrated advantage of SIP is emotional control.

Many beginners:

- panic during market falls,

- delay investing,

- or wait endlessly for “perfect timing.”

SIP reduces this pressure because investing happens automatically and consistently.

Can You Use Both SIP and Lump Sum Together?

Yes.

Many investors combine both methods.

For example:

- investing surplus money through lump sum,

- while continuing monthly SIP investments.

This creates a balance between:

- disciplined investing,

- and immediate capital deployment.

Common Mistakes Beginners Make

Waiting Forever for Perfect Timing

Many people delay investing because they fear market fluctuations.

Investing Large Lump Sum Without Understanding Risk

Market volatility can impact short-term returns significantly.

Stopping SIP During Market Falls

Temporary market declines are a normal part of investing.

Expecting Guaranteed Returns

Both SIP and lump sum investments remain market-linked.

Who Should Choose SIP?

SIP may be suitable for:

- beginners,

- salaried employees,

- long-term investors,

- and investors preferring gradual investing.

Who Should Choose Lump Sum?

Lump sum may suit:

- experienced investors,

- people with large investable funds,

- and investors comfortable with market volatility.

Frequently Asked Questions (FAQs)

Is SIP safer than lump sum?

SIP may reduce market timing risk by spreading investments gradually over time.

Can lump sum give higher returns?

In certain market conditions, lump sum investing may generate higher returns, but risks are also higher.

Is SIP better for beginners?

Many beginners prefer SIP because of smaller investment amounts and disciplined investing structure.

Can I do SIP and lump sum together?

Yes, many investors combine both approaches depending on financial goals and available funds.

Final Thoughts

Both lump sum and SIP investing have their own advantages.

Lump sum investing focuses on:

- immediate investment,

- and higher exposure to current market conditions.

SIP focuses on:

- consistency,

- disciplined investing,

- and gradual wealth building.

Instead of asking:

“Which method is always better?”

it is often more useful to ask:

“Which method matches my financial goals, risk comfort, and investment style?”

For many beginners, SIP is often the simpler and more comfortable starting point for long-term investing.