Introduction

One of the most common questions new investors ask is:

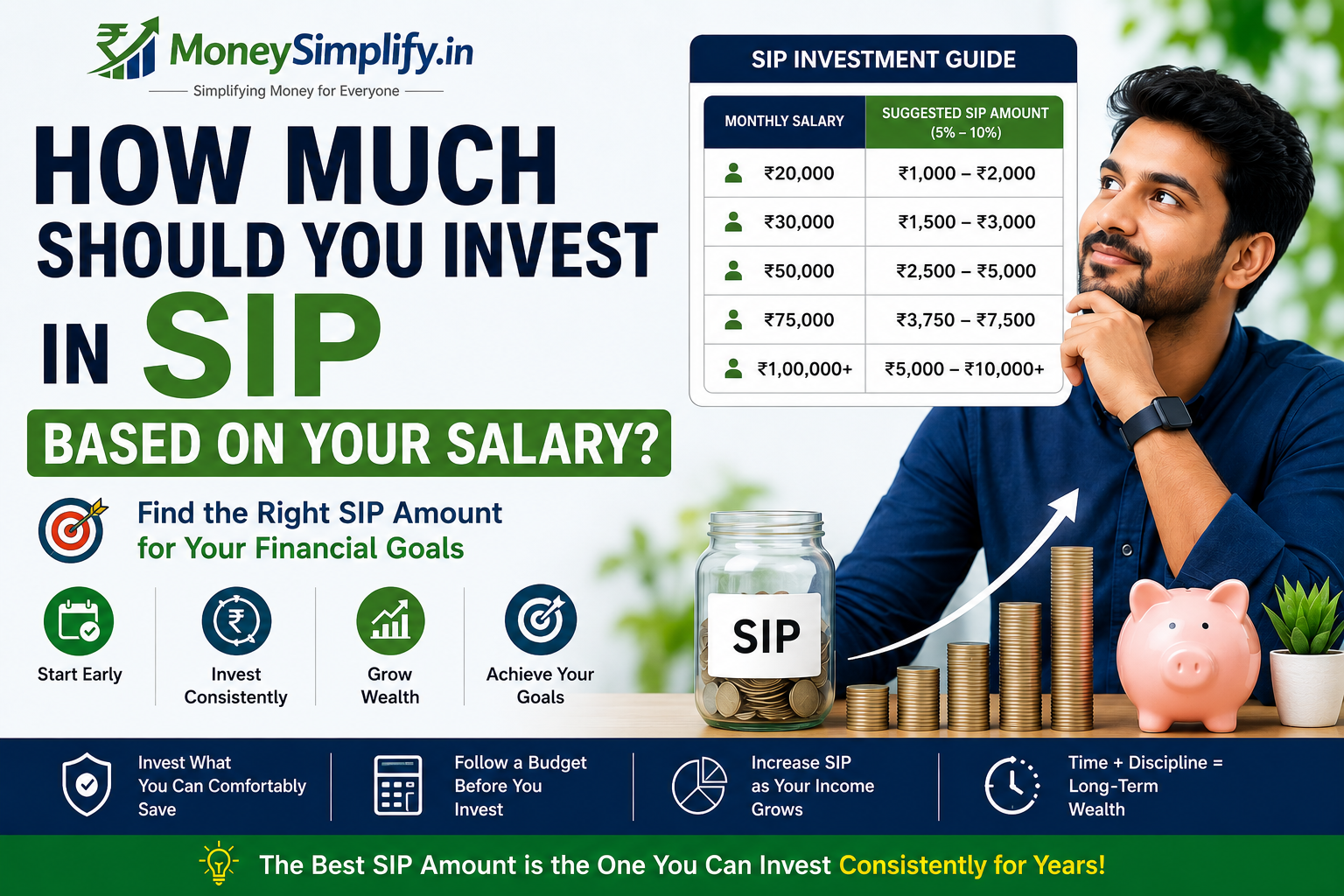

“How much should I invest in SIP?”

Many people assume they need a large salary or substantial savings before they can start investing.

The reality is different.

A SIP can be started with relatively small amounts, and the ideal investment amount depends on your income, expenses, financial goals, and risk tolerance.

Rather than focusing on a fixed number, investors should determine an amount that fits comfortably within their budget while supporting long-term financial goals.

Let’s explore how to decide the right SIP amount based on salary.

Is There a Minimum Salary Required for SIP?

No.

There is no specific salary requirement for starting a SIP.

Many mutual funds allow SIP investments starting from as little as:

- ₹100,

- ₹500,

- or ₹1,000 per month.

The goal is not to invest the largest possible amount immediately.

The goal is to build a consistent investing habit.

Why Your Salary Matters

Your salary influences:

- monthly cash flow,

- savings capacity,

- financial responsibilities,

- and investment potential.

A SIP should never create financial stress.

Before investing, ensure that essential expenses are covered, including:

- housing,

- food,

- transportation,

- insurance,

- and emergency savings.

Investments should be made from surplus income rather than money needed for daily living expenses.

A Simple Rule: Invest a Percentage of Your Income

Many financial planners suggest investing a percentage of income rather than focusing on a fixed amount.

For example:

- 10% of income,

- 15% of income,

- or 20% of income.

The exact percentage depends on individual circumstances.

Starting small and increasing investments over time is often more sustainable than investing aggressively and stopping later.

Use our SIP Calculator to estimate how different monthly investment amounts may potentially grow over time.

SIP Suggestions Based on Salary

The following examples are illustrative and not financial advice.

Salary: ₹20,000 per Month

Possible SIP Range:

- ₹1,000 – ₹2,000

Focus:

- building investing habits,

- creating an emergency fund,

- learning about investing.

Salary: ₹30,000 per Month

Possible SIP Range:

- ₹2,000 – ₹4,000

Focus:

- long-term wealth creation,

- financial discipline,

- gradual portfolio growth.

Salary: ₹50,000 per Month

Possible SIP Range:

- ₹5,000 – ₹10,000

Focus:

- multiple financial goals,

- retirement planning,

- wealth accumulation.

Salary: ₹75,000 per Month

Possible SIP Range:

- ₹7,500 – ₹15,000

Focus:

- accelerating long-term investments,

- goal-based investing,

- diversification.

Salary: ₹1,00,000 per Month

Possible SIP Range:

- ₹10,000 – ₹25,000+

Focus:

- wealth creation,

- retirement planning,

- financial independence goals.

What If You Cannot Invest 10% of Your Salary?

That is perfectly acceptable.

Many beginners start with:

- ₹500,

- ₹1,000,

- or ₹2,000 per month.

The most important factor is consistency.

A smaller SIP maintained for years may be more effective than a large SIP that is stopped after a few months.

Why Starting Early Matters More Than Starting Big

Many investors delay investing because they believe their SIP amount is too small.

However, time is often more important than amount.

Starting earlier provides:

- more compounding opportunities,

- longer investment horizons,

- and greater potential wealth accumulation.

Even modest investments may grow significantly when maintained consistently over long periods.

When Should You Increase Your SIP Amount?

Many investors receive:

- annual salary increments,

- bonuses,

- promotions,

- or additional income.

Instead of increasing lifestyle expenses alone, consider increasing SIP contributions.

A Step-Up SIP strategy allows investors to gradually increase investments over time.

This may help:

- build wealth faster,

- stay ahead of inflation,

- and align investments with income growth.

Common Mistakes to Avoid

Some beginners make mistakes such as:

- investing without an emergency fund,

- choosing unrealistic SIP amounts,

- stopping SIPs during market declines,

- delaying investments unnecessarily,

- and comparing their investments with others.

Investment decisions should be based on personal financial circumstances rather than external comparisons.

Should You Invest More If Markets Fall?

Some investors choose to increase investments during market declines.

Lower market prices may allow SIP contributions to purchase more units.

However, investment decisions should remain aligned with:

- financial goals,

- risk tolerance,

- and overall financial planning.

Avoid making decisions purely based on short-term market movements.

How to Decide Your Ideal SIP Amount

A practical approach is:

Step 1

Calculate monthly income.

Step 2

Subtract essential expenses.

Step 3

Maintain an emergency fund.

Step 4

Determine a comfortable investment amount.

Step 5

Increase SIP contributions gradually as income grows.

This approach helps create a sustainable long-term investing strategy.

Final Thoughts

There is no perfect SIP amount that works for everyone.

The ideal investment amount depends on:

- income,

- expenses,

- financial goals,

- and risk tolerance.

Rather than waiting until you can invest a large amount, consider starting with an amount that comfortably fits your budget.

Over time, consistency, discipline, and gradual increases in investment contributions may play a significant role in long-term wealth creation.

The best SIP amount is not necessarily the largest amount.

It is the amount you can invest consistently for years while staying committed to your financial goals.