Introduction

For many salaried employees, managing monthly expenses, savings, and future financial goals can feel challenging.

After paying for necessities such as rent, groceries, transportation, and bills, many people wonder:

“Can I still invest and build wealth for the future?”

One option often considered by working professionals is a Systematic Investment Plan (SIP).

SIP investing allows salaried employees to invest a fixed amount regularly into mutual funds, helping them build financial discipline and work toward long-term financial goals.

What is SIP?

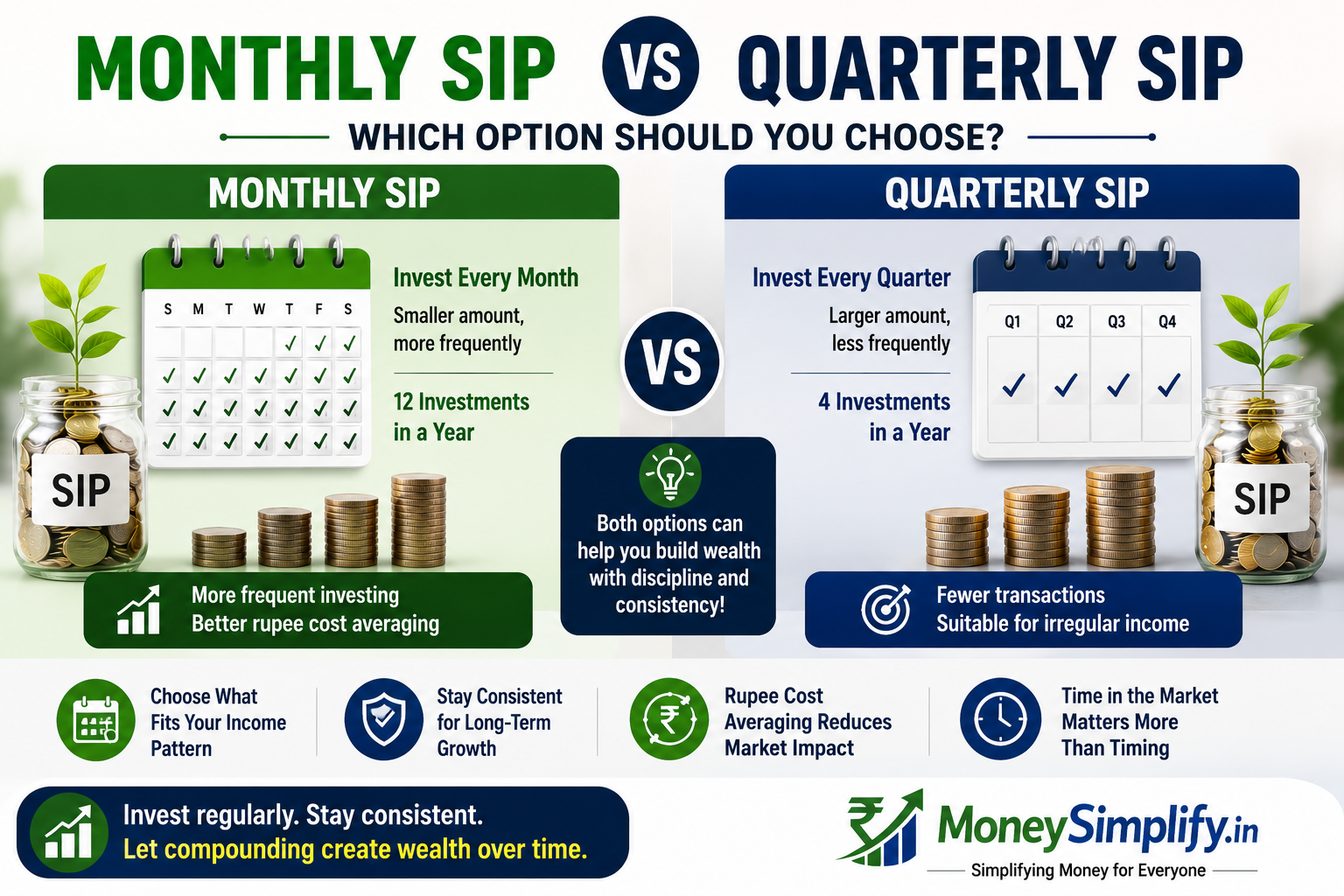

A Systematic Investment Plan (SIP) is a method of investing a fixed amount into mutual funds at regular intervals, usually every month.

Instead of investing a large lump sum amount at once, SIP allows investors to contribute smaller amounts consistently.

This makes SIP particularly attractive for salaried employees who receive a regular monthly income.

You can also use our SIP Calculator to estimate how regular monthly investments may potentially grow over time.

Why SIP is Popular Among Salaried Employees

1. Matches Monthly Salary Cycles

One of the biggest advantages of SIP investing is that it aligns naturally with monthly salary payments.

Many employees schedule SIP deductions shortly after receiving their salary, helping them invest before spending money on non-essential expenses.

This encourages a “save first, spend later” approach.

2. Encourages Financial Discipline

SIP investing promotes consistency.

Since investments are made automatically, salaried employees may avoid the temptation to postpone investing.

Over time, regular investing habits can become an important part of personal financial planning.

3. Helps Build Long-Term Wealth

Many financial goals require long-term planning, such as:

- retirement planning,

- buying a house,

- children’s education,

- wealth creation,

- and financial independence.

SIP investing may help employees work toward these goals through disciplined investing and long-term market participation.

4. Benefits from Compounding

Compounding is one of the most important concepts in long-term investing.

As investments potentially generate returns, those returns may also generate additional returns over time.

The longer investments remain invested, the greater the potential impact of compounding.

This is why many salaried employees start investing as early as possible.

How Much Should Salaried Employees Invest in SIP?

There is no universal amount that works for everyone.

The appropriate SIP amount may depend on:

- monthly income,

- expenses,

- existing savings,

- financial goals,

- and risk tolerance.

Many investors start with an amount they can comfortably continue investing every month.

Consistency is often more important than starting with a large investment amount.

Should Salaried Employees Start SIP Early?

Many investors believe that starting early may be one of the biggest advantages in investing.

A longer investment duration may provide:

- more time for compounding,

- greater investment discipline,

- and better long-term wealth-building opportunities.

Even relatively small SIP amounts may potentially grow significantly when invested consistently over long periods.

Common Financial Goals for Salaried Employees

SIP investing is often used to support goals such as:

Emergency Fund Support

While emergency funds are usually kept in safer savings instruments, SIP investing may complement long-term financial planning.

Retirement Planning

Long-term SIP investing is commonly used for retirement preparation.

Home Purchase Planning

Investors may use SIPs as part of their strategy to accumulate funds for future property purchases.

Financial Independence

Many salaried employees invest with the goal of achieving greater financial freedom over time.

Risks Salaried Employees Should Understand

Although SIP investing may offer several benefits, it is important to understand that mutual funds are market-linked investments.

Risks may include:

- market volatility,

- temporary investment losses,

- poor fund selection,

- and unrealistic return expectations.

Investors should understand both risks and rewards before investing.

Common SIP Mistakes Salaried Employees Should Avoid

Some common mistakes include:

- delaying investments unnecessarily,

- stopping SIPs during market declines,

- investing without financial goals,

- expecting quick profits,

- and investing more than the budget allows.

Maintaining consistency and realistic expectations may help improve long-term investing outcomes.

SIP vs Traditional Saving

Savings accounts and SIPs serve different purposes.

Savings accounts may be suitable for:

- emergency funds,

- short-term expenses,

- and liquidity needs.

SIP investing is generally considered more suitable for:

- long-term wealth creation,

- retirement planning,

- and future financial goals.

Understanding these differences may help investors make better financial decisions.

Final Thoughts

For many salaried employees, SIP investing may provide a practical and disciplined approach to building long-term wealth.

By investing regularly and staying focused on long-term goals, employees may benefit from:

- financial discipline,

- market participation,

- compounding,

- and structured wealth creation.

While SIP investing is not risk-free, it remains a popular choice among working professionals looking to improve their long-term financial future.