Introduction

When planning for long-term financial goals, many investors come across two popular investment options:

- Systematic Investment Plans (SIPs)

- Public Provident Fund (PPF)

Both are widely used in India and offer unique benefits.

However, they work very differently.

This often leads beginners to ask:

“SIP vs PPF: Which investment option is better?”

The answer depends on factors such as:

- risk tolerance,

- investment goals,

- return expectations,

- tax considerations,

- and investment horizon.

Understanding the differences between SIP and PPF can help investors choose the option that aligns best with their financial needs.

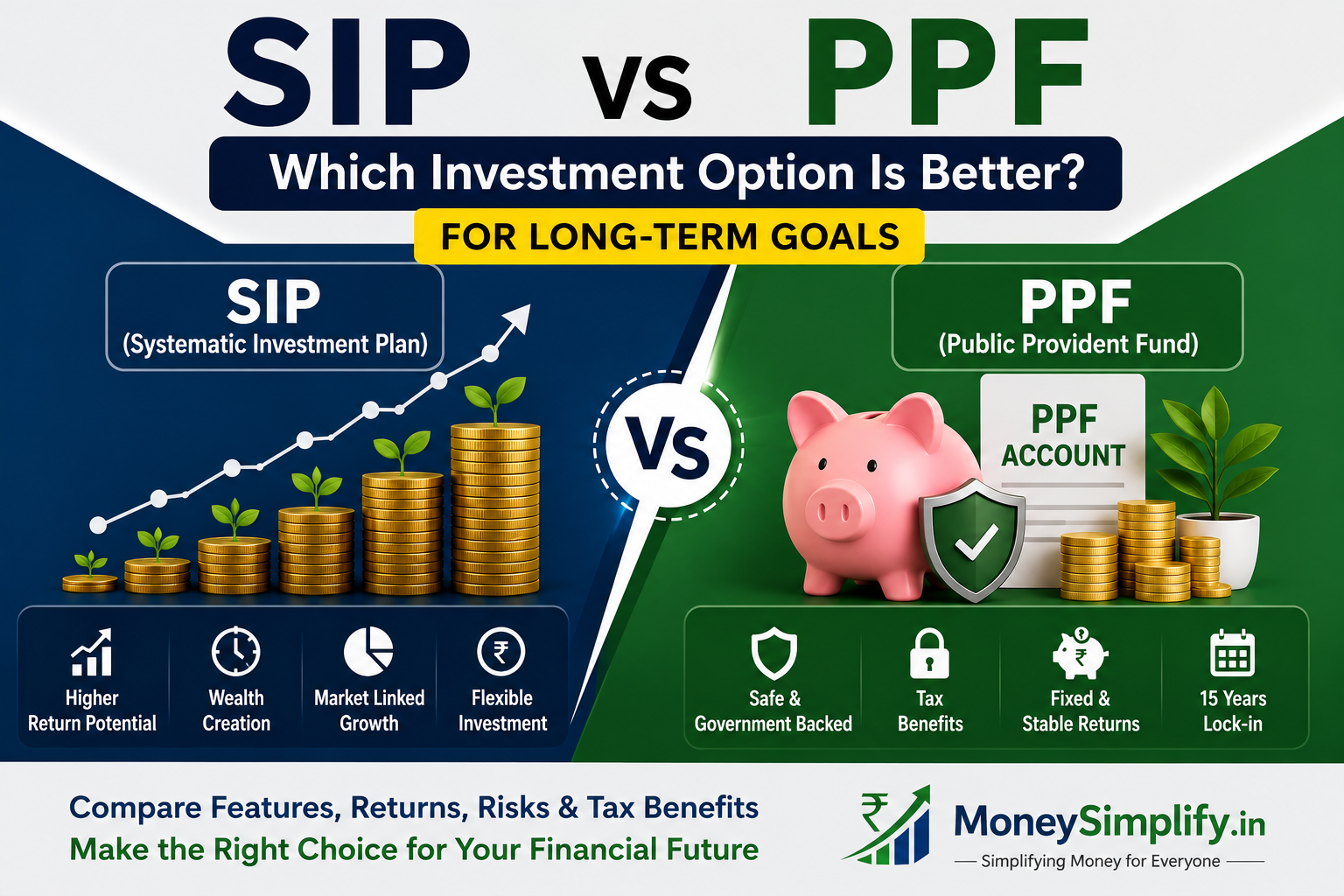

What is SIP?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly into mutual funds.

Instead of investing a large sum at once, SIPs encourage disciplined investing through periodic contributions.

SIPs are commonly used for:

- wealth creation,

- retirement planning,

- children’s education,

- and achieving long-term financial goals.

Returns from SIPs depend on the performance of the mutual funds selected.

You can use our SIP Calculator to estimate potential investment growth over time.

What is PPF?

Public Provident Fund (PPF) is a government-backed long-term savings scheme available in India.

Key features include:

- Government-supported security,

- Fixed interest rates determined periodically,

- 15-year lock-in period,

- Tax benefits under applicable regulations.

PPF is often preferred by conservative investors seeking stability and predictable returns.

SIP vs PPF: Key Differences

| Feature | SIP | PPF |

|---|---|---|

| Investment Type | Mutual Funds | Government Savings Scheme |

| Risk Level | Moderate to High | Very Low |

| Returns | Market-linked | Fixed by Government |

| Return Potential | Higher (not guaranteed) | Moderate and predictable |

| Lock-in Period | Depends on fund type | 15 Years |

| Tax Benefits | Limited to certain funds (ELSS) | Available under applicable rules |

| Inflation Beating Potential | Higher | Moderate |

| Liquidity | Generally Higher | Limited |

Which Option Offers Better Returns?

SIP

SIP returns depend on market performance.

Historically, equity mutual funds have provided the potential for higher long-term returns.

However:

- returns are not guaranteed,

- markets fluctuate,

- and short-term volatility exists.

PPF

PPF offers government-determined interest rates.

Advantages include:

- stable returns,

- low risk,

- and predictable growth.

However, returns may be lower compared to long-term equity investments.

Which Option is Safer?

PPF: Higher Safety

PPF is backed by the Government of India.

Investors seeking:

- capital protection,

- predictable returns,

- and lower risk

often prefer PPF.

SIP: Market-Linked Risk

SIPs invest in mutual funds, making them subject to market fluctuations.

While short-term volatility exists, long-term investing may provide growth opportunities.

Risk tolerance plays an important role when choosing between SIP and PPF.

Can SIP Beat Inflation Better Than PPF?

Inflation reduces purchasing power over time.

Since PPF provides fixed returns, it may struggle to significantly outperform inflation over long periods.

SIPs invested in growth-oriented mutual funds may offer better potential to generate inflation-adjusted returns.

However, higher return potential also involves higher risk.

Which Option is Better for Tax Benefits?

PPF

PPF is known for its tax advantages.

It generally offers benefits related to:

- contributions,

- interest earned,

- and maturity proceeds,

subject to prevailing tax laws.

SIP

Tax benefits are typically available only through specific mutual fund categories such as ELSS funds.

Regular equity mutual fund SIPs primarily focus on wealth creation rather than tax savings.

Investors should consult updated tax regulations before making decisions.

Who Should Choose SIP?

SIP may be suitable for investors who:

- have long-term financial goals,

- can tolerate market fluctuations,

- seek higher wealth creation potential,

- and want inflation-beating opportunities.

Examples:

- retirement planning,

- children’s higher education,

- long-term wealth accumulation.

Who Should Choose PPF?

PPF may be suitable for individuals who:

- prefer low-risk investments,

- prioritize capital safety,

- seek tax-efficient savings,

- and are comfortable with long lock-in periods.

Examples:

- conservative retirement planning,

- stable long-term savings goals.

Can You Invest in Both SIP and PPF?

Yes.

Many investors combine SIP and PPF to balance:

SIP

For:

- growth,

- wealth creation,

- inflation protection.

PPF

For:

- stability,

- safety,

- tax-efficient savings.

Combining both may provide diversification and support different financial objectives.

Common Mistakes to Avoid

Some investors make mistakes such as:

- assuming SIP returns are guaranteed,

- expecting PPF to generate high wealth growth,

- ignoring inflation,

- investing without clear goals,

- and choosing investments solely based on popularity.

Selecting investments based on personal financial circumstances is important.

SIP vs PPF: Which is Better?

SIP may be better if you:

✓ Want higher long-term growth potential

✓ Can tolerate market volatility

✓ Aim to beat inflation

✓ Have long investment horizons.

PPF may be better if you:

✓ Prioritize safety and stability

✓ Prefer predictable returns

✓ Seek government-backed savings

✓ Want tax-efficient long-term savings.

Final Thoughts

There is no universal winner between SIP and PPF.

Both serve different purposes.

If your priority is long-term wealth creation and inflation-beating potential, SIPs may be more suitable.

If you prefer safety, predictability, and government-backed savings, PPF may align better with your needs.

Many investors successfully use both options together to create a balanced financial plan.

Before investing, consider:

- your financial goals,

- risk tolerance,

- investment horizon,

- and overall financial strategy.

The best investment option is the one that supports your unique financial journey.