If you’ve started investing in mutual funds, you may have noticed that almost every mutual fund scheme offers two options:

- Direct Plan

- Regular Plan

Many beginners naturally wonder:

“Which option should I choose? Are Direct Mutual Funds better than Regular Mutual Funds?”

The answer isn’t as simple as saying one is always better than the other.

While Direct Plans generally have lower costs, Regular Plans may offer professional guidance and support through distributors or financial advisors.

In this guide, we’ll explain the differences between Direct and Regular Mutual Funds in simple language so you can make an informed decision based on your own investing needs.

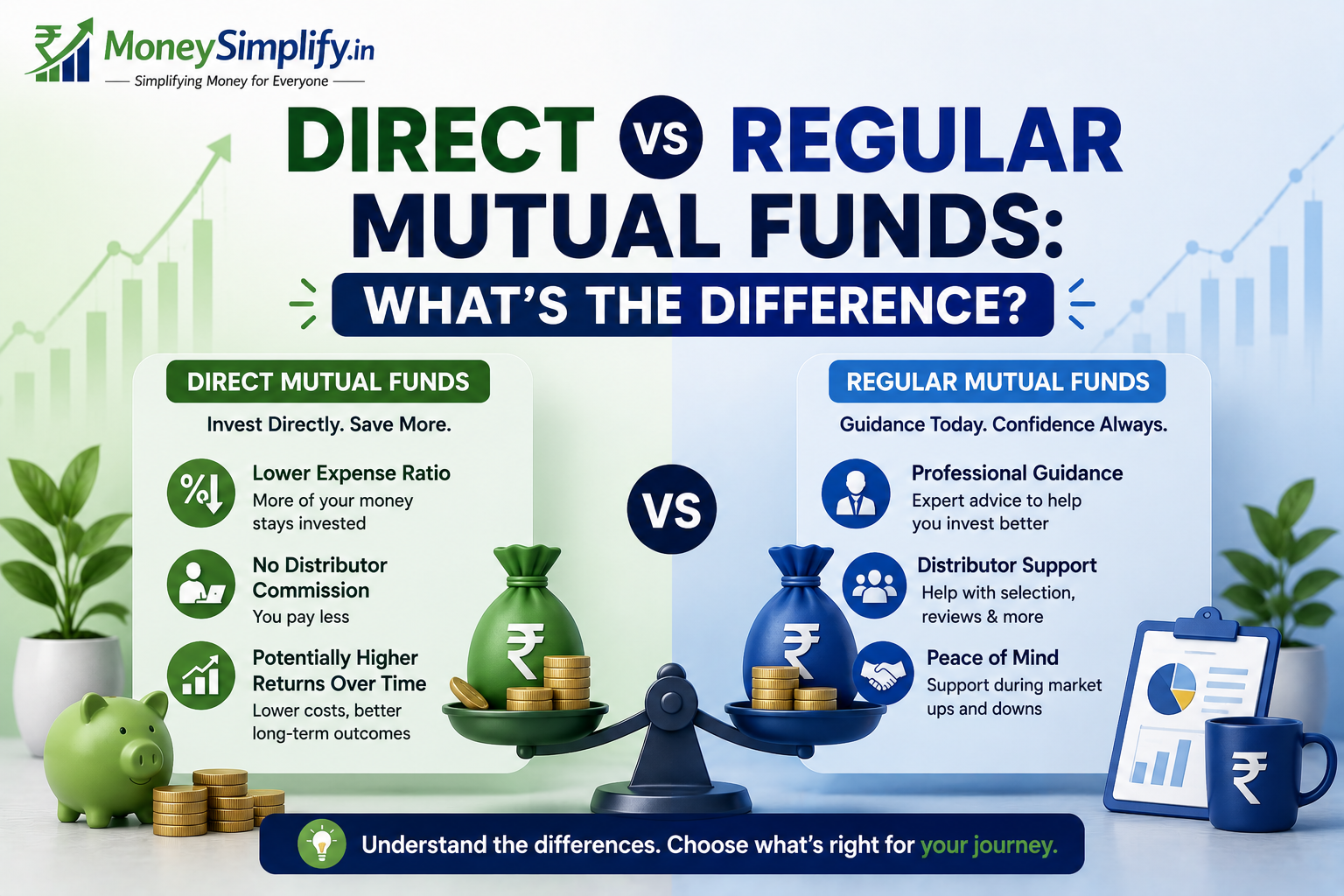

What Are Direct Mutual Funds?

Direct Mutual Funds are mutual fund plans that investors purchase directly from the Asset Management Company (AMC) without involving any intermediary, distributor, or agent.

Since there is no distributor involved, the fund house does not pay commissions.

As a result:

Direct Plans usually have lower expense ratios compared to Regular Plans.

Example

Suppose you decide to invest in a mutual fund through the AMC’s website or a direct investment platform.

Since no intermediary is involved, you’re investing through the Direct Plan.

Characteristics of Direct Mutual Funds

- Purchased directly from the mutual fund company.

- Lower expense ratios.

- Potentially higher returns over the long term due to lower costs.

- Suitable for investors comfortable managing investments independently.

What Are Regular Mutual Funds?

Regular Mutual Funds are purchased through distributors, agents, banks, brokers, or financial advisors.

In this arrangement, the distributor receives a commission from the AMC for facilitating the investment.

This commission is included within the expense ratio.

Therefore:

Regular Plans generally have slightly higher expense ratios than Direct Plans.

Example

If you invest through a bank relationship manager or mutual fund advisor who helps you select schemes and complete the process, you’re likely investing through a Regular Plan.

Characteristics of Regular Mutual Funds

- Purchased through intermediaries.

- Include distributor commissions.

- Higher expense ratios compared to Direct Plans.

- May provide access to investment guidance and support.

Direct vs Regular Mutual Funds: Key Differences

| Feature | Direct Mutual Funds | Regular Mutual Funds |

|---|---|---|

| Purchase Method | Directly through AMC | Through distributor/advisor |

| Distributor Involvement | No | Yes |

| Expense Ratio | Lower | Higher |

| Commissions | No distributor commission | Includes distributor commission |

| Professional Guidance | Usually self-managed | Advisor/distributor support |

| Return Potential | Slightly higher due to lower costs | Slightly lower due to higher expenses |

| Suitable For | DIY investors | Investors seeking guidance |

Understanding Expense Ratio

One of the biggest differences between Direct and Regular Plans is the expense ratio.

Expense ratio refers to:

The annual fee charged by the mutual fund to manage your investments.

This fee covers:

- Fund management expenses

- Administrative costs

- Marketing expenses

- Distributor commissions (in Regular Plans)

Since Direct Plans eliminate distributor commissions, their expense ratios are usually lower.

Why Does Expense Ratio Matter?

At first glance, the difference may seem small.

For example:

- Direct Plan Expense Ratio: 1.0%

- Regular Plan Expense Ratio: 1.5%

The difference is only 0.5% annually.

However, due to the power of compounding, even small cost differences can have a noticeable impact over long investment periods.

Example: Direct vs Regular Mutual Funds

Suppose two investors each invest:

- Monthly SIP: ₹10,000

- Investment Period: 20 years

- Expected Return Before Expenses: 12%

Investor A: Direct Plan

Effective Return After Expenses: 11.5%

Investor B: Regular Plan

Effective Return After Expenses: 11.0%

Over 20 years, Investor A may accumulate a larger corpus because of lower ongoing expenses.

This example highlights an important principle:

Reducing costs can potentially improve long-term investment outcomes.

However, cost should not be the only factor when choosing between Direct and Regular Plans.

Is Lower Cost Always Better?

Not necessarily.

While Direct Plans often offer lower costs, some investors value professional support.

For example:

A beginner investor may benefit from guidance related to:

- Asset allocation

- Fund selection

- Portfolio reviews

- Financial goal planning

- Staying disciplined during market volatility

If professional advice helps an investor avoid emotional decisions, the additional cost of a Regular Plan may be worthwhile for some individuals.

Things to Remember

Direct Mutual Funds

Advantages:

- Lower expense ratios.

- Potentially better long-term returns.

- Greater control over investment decisions.

Considerations:

- Requires research and self-management.

- Investors must monitor their portfolios independently.

Regular Mutual Funds

Advantages:

- Professional guidance and support.

- Assistance with investment selection.

- Useful for beginners seeking advice.

Considerations:

- Higher expense ratios.

- Slightly lower return potential due to additional costs.

A Simple Analogy

Think of booking a vacation.

Direct Plan

You plan everything yourself:

- Flights

- Hotels

- Itinerary

You may save money but need to invest time and effort.

Regular Plan

You use a travel agent.

You pay a little extra, but receive assistance and guidance throughout the process.

Neither approach is universally better.

The right choice depends on your comfort level and preferences.

In the next section, we’ll discuss who may prefer Direct Plans, who may benefit from Regular Plans, common FAQs, and how to choose the option that aligns best with your financial journey.

Who May Prefer Direct Mutual Funds?

Direct Mutual Funds may be suitable for investors who:

- Enjoy researching investment options independently.

- Understand mutual fund concepts and risk profiles.

- Are comfortable selecting and reviewing funds themselves.

- Want to minimize investment costs through lower expense ratios.

- Prefer managing their own financial decisions.

Example

Rahul has been investing for several years. He regularly reads about mutual funds, understands asset allocation, and reviews his portfolio annually.

Since he is comfortable making investment decisions independently, Direct Mutual Funds may align well with his approach.

Who May Prefer Regular Mutual Funds?

Regular Mutual Funds may be suitable for investors who:

- Are new to investing.

- Prefer professional guidance.

- Need help choosing suitable mutual funds.

- Want assistance with financial planning and goal setting.

- Feel more confident having an advisor to consult during market fluctuations.

Example

Priya is investing for the first time. She feels uncertain about selecting funds and understanding market conditions.

In her case, working with a qualified advisor through a Regular Plan may provide reassurance and support.

Should Beginners Choose Direct or Regular Plans?

There is no single answer that applies to everyone.

Beginners May Consider Direct Plans If:

- They are willing to learn about investing.

- They have access to reliable educational resources.

- They feel comfortable making independent decisions.

Beginners May Consider Regular Plans If:

- They prefer professional assistance.

- They value personalized guidance.

- They feel overwhelmed by investment choices.

Remember:

The best mutual fund plan is the one that helps you stay invested consistently and make informed decisions.

Can You Switch from Regular to Direct Mutual Funds?

Yes.

Investors can switch from Regular Plans to Direct Plans.

However, before making any changes, it’s important to understand:

- Potential tax implications.

- Exit loads, if applicable.

- Whether you still require professional advice.

If you’re unsure, consider consulting a qualified financial advisor before switching.

Common Misconceptions About Direct and Regular Mutual Funds

Myth 1: Direct Plans Are Always Better

Fact:

Direct Plans generally have lower costs, but they may not be ideal for investors who need guidance and support.

Myth 2: Regular Plans Are Bad Investments

Fact:

Regular Plans invest in the same underlying mutual fund schemes. The primary difference lies in expenses and distribution support.

Myth 3: Returns Are Completely Different

Fact:

Both plans invest in the same portfolio. The difference in returns usually arises from differences in expense ratios.

Myth 4: Beginners Should Avoid Direct Plans

Fact:

Many beginners successfully invest through Direct Plans after educating themselves about investing principles.

Frequently Asked Questions (FAQs)

What is the main difference between Direct and Regular Mutual Funds?

The primary difference is that Direct Plans are purchased directly from the Asset Management Company without intermediaries, while Regular Plans involve distributors or advisors who receive commissions.

Do Direct Mutual Funds offer higher returns?

Direct Plans generally have lower expense ratios, which may result in slightly higher returns over long investment periods.

However, returns are not guaranteed.

Are Direct and Regular Mutual Funds invested in different portfolios?

No.

Both Direct and Regular Plans invest in the same underlying mutual fund portfolio.

The main difference is the expense ratio.

Are Regular Mutual Funds expensive?

Regular Plans usually have higher expense ratios because they include distributor commissions.

Whether the additional cost is worthwhile depends on the value of the advice and support received.

Can I switch from Regular Plans to Direct Plans later?

Yes.

However, investors should understand any applicable tax implications and exit loads before switching.

Which option is better for beginners?

It depends.

Beginners who are comfortable learning and managing investments independently may prefer Direct Plans.

Those seeking guidance and support may find Regular Plans more suitable.

Helpful Tools for Mutual Fund Investors

If you’re planning your mutual fund investments through SIPs, these calculators may help estimate potential outcomes:

SIP Calculator

Use our SIP Calculator to estimate how your monthly investments may grow over time and support your long-term financial goals.

Step-Up SIP Calculator

Expect your income to increase in the future? Try our Step-Up SIP Calculator to understand how increasing your SIP amount annually may potentially accelerate wealth creation.

Crorepati SIP Calculator

Want to build a ₹1 Crore corpus? Our Crorepati SIP Calculator can help estimate the monthly SIP amount required to work toward this milestone.

Final Thoughts

The decision between Direct and Regular Mutual Funds isn’t about finding a universally “better” option.

Instead, it’s about understanding:

- How comfortable you are managing investments independently.

- Whether professional guidance adds value for your situation.

- The impact of costs on long-term investing outcomes.

Direct Plans may appeal to investors who prefer a hands-on approach and lower expenses.

Regular Plans may benefit investors who value advice, support, and assistance with financial planning.

The most important factor is not whether you choose Direct or Regular Plans.

Rather, it’s developing the habit of investing consistently, staying focused on your financial goals, and continuing to improve your understanding of personal finance over time.

Remember:

Successful investing is often less about choosing the perfect plan and more about maintaining discipline and making informed decisions over the long term.

Disclaimer: Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. This article is intended for educational purposes only and should not be considered financial advice.