If you’ve recently started learning about mutual funds, you may have noticed that there are many different types available. Terms like equity funds, debt funds, hybrid funds, and index funds can seem confusing at first.

A common question many beginners ask is:

“Which type of mutual fund should I choose?”

The truth is that there is no single mutual fund category that is perfect for everyone. The right choice depends on your financial goals, investment timeline, and comfort with risk.

In this guide, we’ll explain the major types of mutual funds in simple language so you can better understand how they work and which ones might align with your investment objectives.

Why Are There Different Types of Mutual Funds?

Think about two investors:

- Rahul, who is 25 years old, wants to build wealth for retirement and is comfortable with market fluctuations.

- Priya, who plans to use her money for a house down payment in three years and prefers stability.

Would both investors choose the same type of mutual fund?

Probably not.

Different mutual fund categories exist because investors have different goals, time horizons, and risk appetites. Some funds focus on growth, while others prioritize stability or tax savings.

Understanding these categories is the first step toward making informed investment decisions.

1. Equity Mutual Funds

Equity mutual funds primarily invest in stocks of companies listed on stock exchanges.

Simply put, when you invest in an equity mutual fund, you indirectly become a small owner in many companies through a professionally managed portfolio.

Who Are Equity Funds Suitable For?

Equity funds are generally suitable for investors who:

- Have long-term financial goals.

- Can tolerate short-term market fluctuations.

- Want to build wealth over time.

Example

Suppose you’re 28 years old and planning for retirement 30 years from now. Since you have a long investment horizon, equity funds may offer the potential for long-term growth despite short-term market ups and downs.

Types of Equity Funds

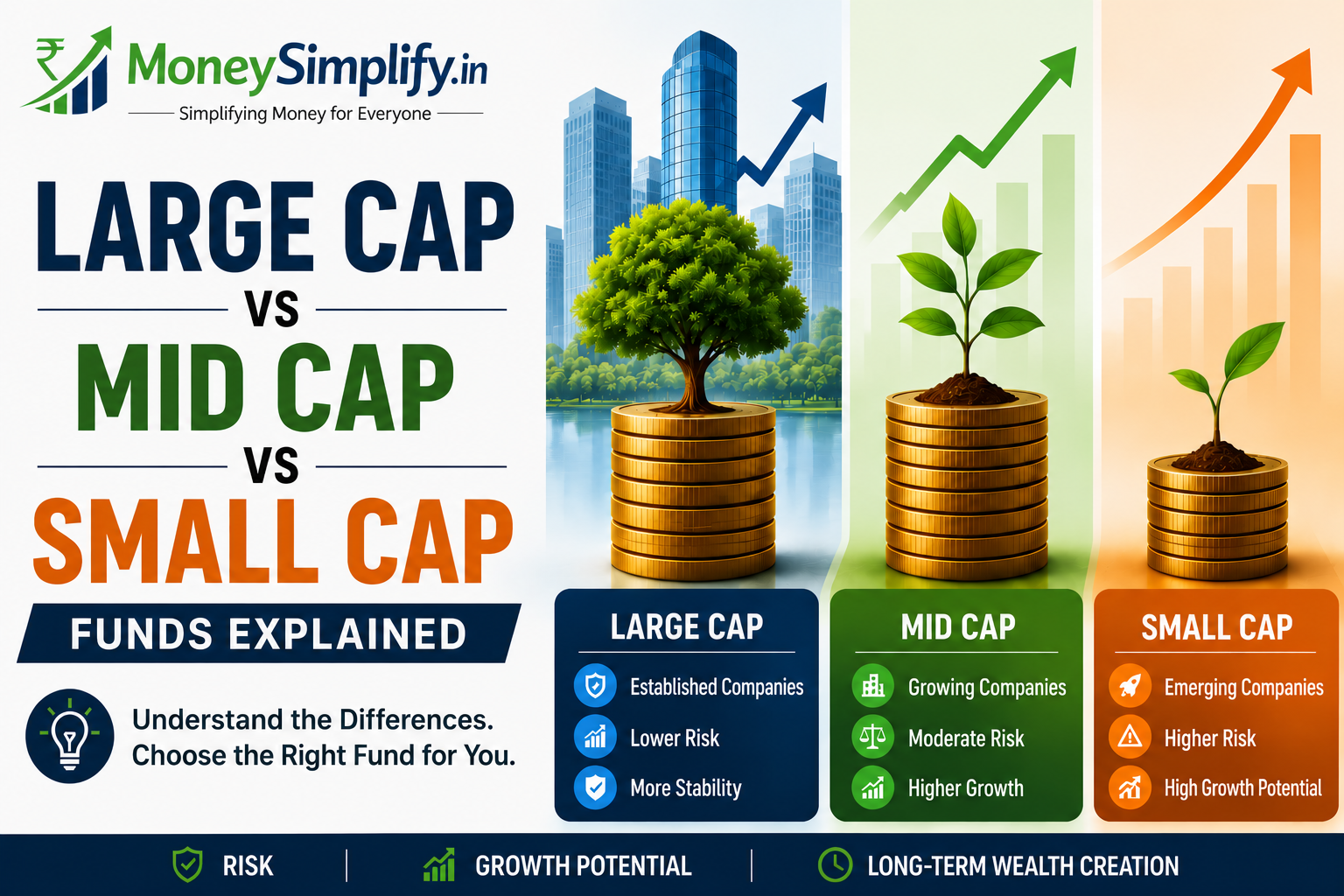

Large-Cap Funds

These funds invest in well-established companies with large market capitalizations.

Examples may include companies that are leaders in their industries.

Suitable for:

- Beginners seeking relatively stable equity exposure.

- Long-term investors.

Mid-Cap Funds

Mid-cap funds invest in medium-sized companies that may have higher growth potential.

However, they can also be more volatile than large-cap funds.

Suitable for:

- Investors willing to take moderate risk.

- Long-term investors seeking growth opportunities.

Small-Cap Funds

These funds invest in smaller companies with significant growth potential.

They may generate higher returns over the long term but often experience greater volatility.

Suitable for:

- Experienced investors.

- Investors with high risk tolerance.

Multi-Cap Funds

Multi-cap funds invest across large-cap, mid-cap, and small-cap companies.

This diversification allows exposure to different segments of the market.

Suitable for:

- Investors seeking diversified equity exposure.

Advantages of Equity Funds

- Potential for long-term wealth creation.

- Opportunity to benefit from economic growth.

- Diversification across multiple companies.

- Professional fund management.

Things to Remember

Equity funds can experience significant short-term fluctuations.

If market volatility makes you uncomfortable, it may be important to assess whether a high equity allocation suits your risk tolerance.

2. Debt Mutual Funds

Debt mutual funds invest in fixed-income instruments such as government securities, treasury bills, and corporate bonds.

Think of debt funds as a category designed to provide relatively more stability compared to equity funds.

Who Are Debt Funds Suitable For?

Debt funds may be appropriate for investors who:

- Prefer lower risk.

- Have short- to medium-term goals.

- Want relatively stable returns.

Example

Imagine you’re planning to use your savings for a vacation in two years. Since preserving your capital may be more important than aggressive growth, debt funds could be worth considering.

Types of Debt Funds

Liquid Funds

These invest in very short-term debt instruments.

Suitable for:

- Emergency funds.

- Parking surplus money temporarily.

Short Duration Funds

These funds invest in debt securities with shorter maturities.

Suitable for:

- Investors with short-term goals.

Corporate Bond Funds

These funds primarily invest in bonds issued by companies.

Suitable for:

- Investors seeking moderate income potential.

Gilt Funds

Gilt funds invest mainly in government securities.

Since they are backed by government instruments, credit risk is generally lower.

Advantages of Debt Funds

- Lower volatility compared to equity funds.

- Better liquidity than some traditional products.

- Suitable for conservative investors.

Things to Remember

Debt funds are not entirely risk-free.

They can be affected by:

- Interest rate changes.

- Credit risk.

- Market conditions.

3. Hybrid Mutual Funds

Hybrid mutual funds combine equity and debt investments within a single fund.

You can think of them as a middle ground between growth and stability.

Who Are Hybrid Funds Suitable For?

Hybrid funds may be suitable for:

- First-time investors.

- Moderate risk investors.

- Investors seeking diversification.

Example

Suppose you’re new to investing and feel uncomfortable putting all your money into equities.

A hybrid fund may provide exposure to equities for growth while maintaining debt exposure for stability.

Types of Hybrid Funds

Aggressive Hybrid Funds

These funds allocate a larger portion to equities.

Suitable for:

- Investors comfortable with moderate to high risk.

Conservative Hybrid Funds

These allocate more money toward debt instruments.

Suitable for:

- Conservative investors.

Balanced Advantage Funds

These funds dynamically adjust allocations between equity and debt depending on market conditions.

Advantages of Hybrid Funds

- Diversification across asset classes.

- Reduced volatility compared to pure equity funds.

- Simpler portfolio management.

Things to Remember

Hybrid funds may generate lower returns than pure equity funds during strong bull markets.

However, they may also help reduce downside risk.

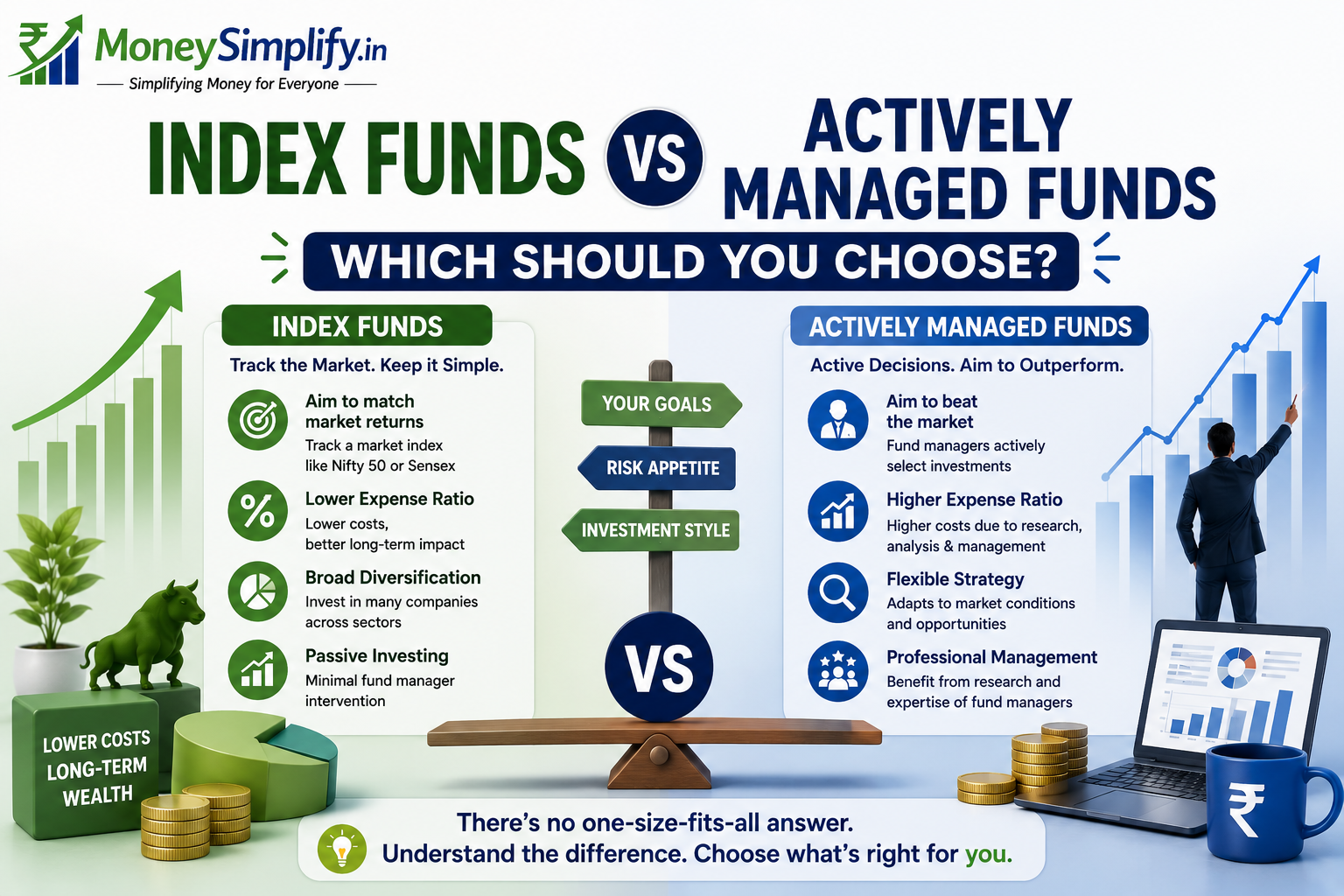

4. Index Funds

Index funds aim to replicate the performance of a specific market index, such as the Nifty 50 or Sensex.

Instead of trying to outperform the market, these funds attempt to match market performance.

Who Are Index Funds Suitable For?

Index funds may be suitable for:

- Beginners.

- Passive investors.

- Long-term investors.

Example

Imagine you simply want your investments to grow alongside the broader market without actively selecting funds.

Index funds offer a straightforward approach to investing.

Advantages of Index Funds

- Lower expense ratios.

- Broad diversification.

- Simplicity.

- Reduced dependence on fund manager decisions.

Things to Remember

Index funds will generally perform in line with the market.

They are unlikely to significantly outperform the index they track.

5. ELSS (Equity Linked Savings Scheme)

ELSS funds are tax-saving mutual funds that qualify for deductions under Section 80C of the Income Tax Act.

These funds primarily invest in equities and come with a lock-in period of three years.

Who Are ELSS Funds Suitable For?

ELSS funds may be suitable for investors who:

- Want tax-saving benefits.

- Have long-term goals.

- Are comfortable with equity market risks.

Example

Suppose you want to reduce your taxable income while also investing for long-term wealth creation.

ELSS funds may help achieve both objectives.

Advantages of ELSS Funds

- Tax deduction benefits.

- Equity exposure for growth potential.

- Shorter lock-in period compared to some tax-saving alternatives.

Things to Remember

ELSS funds are still equity investments and remain subject to market risks.

Which Mutual Fund Type Is Right for You?

The best mutual fund depends on your personal circumstances.

Consider Equity Funds If:

- You have goals more than 5–7 years away.

- You can tolerate market fluctuations.

- Wealth creation is your primary objective.

Consider Debt Funds If:

- Capital preservation is important.

- You have short-term goals.

- You prefer relatively stable investments.

Consider Hybrid Funds If:

- You want a balanced approach.

- You’re a beginner investor.

- Moderate risk suits your comfort level.

Consider Index Funds If:

- You prefer passive investing.

- You value simplicity and lower costs.

- You want broad market exposure.

Consider ELSS Funds If:

- Tax savings are important.

- You have a long-term investment horizon.

Frequently Asked Questions (FAQs)

Which mutual fund is best for beginners?

Hybrid funds and index funds are often considered beginner-friendly because they offer diversification and moderate risk exposure.

Are equity mutual funds risky?

Yes. Equity funds are subject to market fluctuations and may experience short-term volatility.

Are debt funds completely safe?

No investment is completely risk-free. Debt funds generally carry lower risk than equity funds but may still be affected by interest rate and credit risks.

Can I invest in multiple mutual fund categories?

Yes. Many investors diversify their portfolios by investing across different fund categories based on their goals.

Which mutual fund provides tax benefits?

ELSS funds offer tax deductions under Section 80C of the Income Tax Act.

Final Thoughts

Choosing a mutual fund doesn’t have to be complicated.

Instead of searching for the “best” mutual fund, focus on finding funds that align with your financial goals, investment horizon, and comfort with risk.

Remember that investing is a journey, not a race. Understanding the different types of mutual funds can help you make more confident decisions and build a portfolio that supports your long-term objectives.

If you’re just starting out, it’s perfectly normal to begin with simpler options such as index funds or hybrid funds and gradually expand your knowledge over time.

If you’re planning to invest regularly in mutual funds, try our SIP Calculator to estimate how your monthly investments may grow over time and support your long-term financial goals.

Expect your income to increase over the years? Use our Step-Up SIP Calculator to understand how gradually increasing your SIP contributions may potentially accelerate wealth creation.

If your goal is to build a ₹1 Crore corpus through disciplined investing, our Crorepati SIP Calculator can help estimate the monthly SIP amount needed to work toward that milestone.

Disclaimer: Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. This article is for educational purposes only and should not be considered financial advice.